No Brexit hasn't been a disaster

Chillax, we're still just as bad as the rest of Europe

The recent visit to the UK by French President Emmanuel Macron was a classic in the grand tradition of Anglo-French diplomacy. There was the usual faded grandeur and formal ceremony expected of two venerable European states and failed empires.

There was also the ancient right of explaining to the host everything wrong in their country.

Macron lived up to this and reminded us why the French have a cockerel as a national symbol, happy to crow about itself even though it's up to its ankles in s—t and ultimately heading for the chopper. France is, on nearly every objective measure, doing worse than the UK. It just gets to hide in a bigger bond market.

Chart: Under Macron’s inspired leadership, French spreads continue to go higher

And, of course, despite his disastrous handling of the Brexit talks, which history tells us will haunt UK-EU relations for decades, Macron proceeded to explain why all the Brits’ problems were due to Brexit.

As usual, Macron was wrong.

"There are two kinds of Europeans: The smart ones, and those who stayed behind." - H.L. Mencken

Despite the UK voting to leave 9 years ago and actually leaving 4 years ago, I often get subjected to lengthy pro-EU rants at events or online. So I thought I would do what they haven’t bothered to do, which is look at the facts and the history.

Before I begin, I need to clarify that I am strongly in favour of increased European cooperation.

What I want to emphasise is that, despite the EU's attempts to hide behind this, the EU isn’t Europe, and it’s a flawed model that has, unsurprisingly, done a terrible job. We know this because it repeatedly tells us this itself, most recently in the Draghi report.

There must be a recognition that many of the UK's failures are of its own making. The EU didn’t help, but it wasn’t the primary cause.

So this is the first in a series of notes which cover:

Why Brexit hasn’t been a disaster.

Why Brexit was probably inevitable.

What’s going wrong with the EU in its own words.

Why the EU is increasingly resembling other failed European superstates.

No, Brexit hasn’t been a disaster

“The only function of economic forecasting is to make astrology look respectable.” ―John Kenneth Galbraith

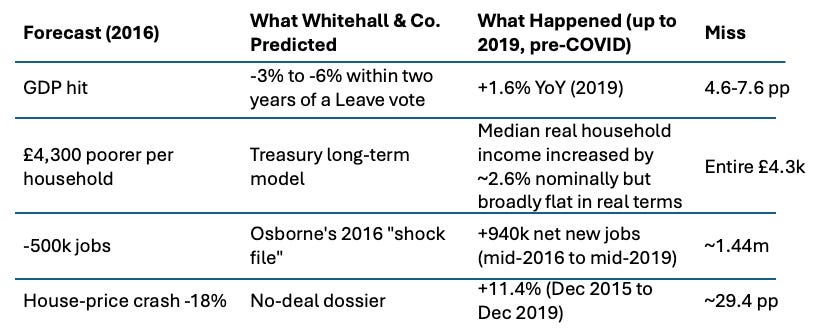

Remember those dire government predictions before the vote? GDP falling off a cliff, house prices crashing, half a million jobs lost. The airwaves were thick with it. And yet, here we are in 2025, and the reality looks… different.

Take a look at what was promised versus what actually happened:

The much-anticipated economic disaster didn’t happen, and the dire predictions by many didn’t come true. This is mainly because the economic case for the EU, from the UK’s perspective, was always weak, and I will cover this in another note.

I fully accept there may have been other reasons for being a member, but the economic case was always suspect. We know this because we have the data, plus the government papers from the 1970s have been declassified.

The £100 Billion Illusion: Economysticism at its finest

Undeterred by their previous failure, the die-hard Euro-augurs haven’t let up, and we now have the much-touted £100 billion a year cost.

Unbelievably, despite the obvious holes in this number, I have been confidently quoted this number by senior financial types in the City, who should know better.

I could understand this in public, as I know from personal experience, there is a long tradition of governments quashing dissent by the sellside when they point out the obvious.

This is especially true of the EU and its ever-growing web of off-balance sheet borrowing vehicles that hand out regular bond mandates.

This £100bn figure is thrown around like gospel, but it’s built on sand, designed to distract from a broader, more uncomfortable truth for EU fanatics: the UK's economic performance is, frankly, much like the EU's – pretty poor.

The first starting point for this number is the OBR, which, as we all know, is hardly a bastion of quality forecasting itself. There are also issues with their number, which is based on lost productivity over a 15-year period. That said, some of which are not the fault of the OBR, to be fair.

However, the more recent and, in my opinion, deeply dishonest piece of work is by a privately owned US media company, Bloomberg. However, there are just a few issues with this.

The choice of peers:

The synthetic-control (“doppelganger”) technique that Bloomberg leans on is a basket of “comparable” countries. I could not find the exact basket used by Bloomberg, but the usual ones are the OECD or a ’weighted G7’. Whilst not unreasonable as a thought exercise, it’s not exactly robust either. As every data scientist knows, the problem with both control pools is: Why those peers? Why those weights and why those start and end dates? All of these change the headline loss by several points.

When the economist Julian Jessop (a Brexiteer) swaps the US-heavy doppelganger for the euro-area average, the gap shrinks to about £25 bn—far below Bloomberg’s figure and a 1% loss.This seems much more reasonable. Brexit was always going to be a shock and, at least in the short term, a cost to the economy. Comparing the performance of the UK to the rest of Europe, it looks about where you would expect it to be.

It’s Covid, stupid

This, for me, is the big one. The work also treats every post-2016 gap between the UK and its comparator basket as a Brexit effect. This assumes COVID-19 and the energy crisis struck every country equally. COVID was an immense shock to the global economy.

Yet, there were very different approaches to lockdown, and the UK’s aerospace, automotive, and energy-intensive sectors were hit harder than their peers, meaning much of the measured shortfall would have occurred even without Brexit. The UK has also made a series of really bad economic decisions entirely of its own.

One-sided balance sheet:

It presumes the shock is irreversible. Potential upsides—such as new trade deals, regulatory changes, and a rebound in deferred investment—are omitted, so the calculation can only be negative.

Britain vs. Europe: Excessive regulation isn’t a superpower

This comparison with the EU is key. The "Brexit penalty" is indistinguishable from continental drift. To pin £100 billion on Brexit alone is to wilfully ignore the shared issues and the minimal amount of actual divergence that has occurred. Something even Trump has repeatedly mentioned.

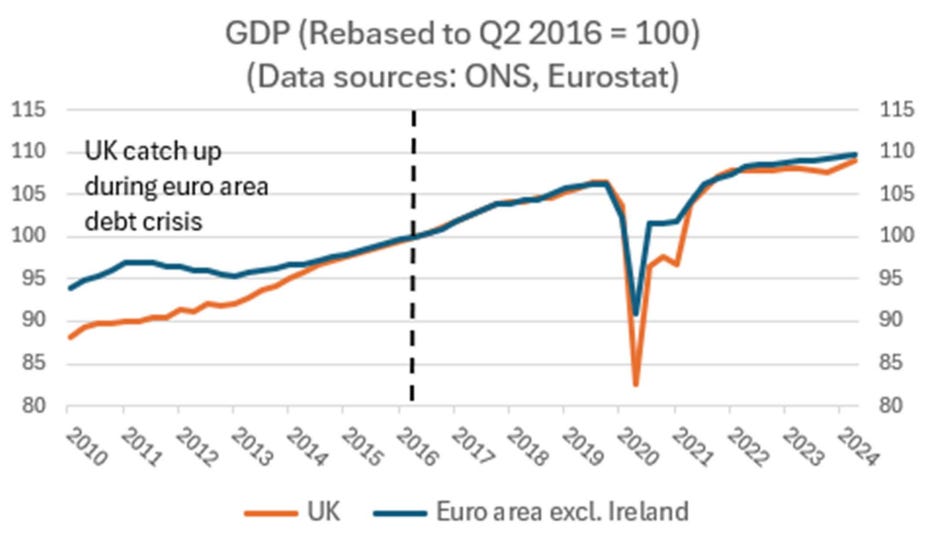

The UK's performance, when viewed in comparison to its European peers, suggests common structural issues rather than a unique "Brexit cost."

Chart: The UK’s performance over Covid hasn’t been good, but was returning to trend

Source: Julian Jessop

These are not the figures of an economy uniquely crippled by a singular event. These are the figures of a developed economy facing the same global challenges and structural deficiencies as the rest of the EU.

Chart: Allegedly, the UK faces a brighter future, but I suspect this will be wrong too (Thanks, Rach)

Dr Draghi’s Dire Diagnosis

“When someone shows you who they are, believe them the first time.” - Maya Angelou

The EU prides itself as a regulatory superpower. This isn’t a superpower; it’s economic kryptonite. High degrees of regulation benefit large, slow-growing incumbents while crushing smaller firms and stifling innovation. The EU’s recent AI legislation is a good example of that.

Recently, Mario Draghi joined a long list of EU luminaries (Delors 89, Saphir 03, Kok 04, Monti 10, Four Presidents 12, Five Presidents! 15 and Letta 24) in publishing a report detailing the EU’s problems and what needs to be done.

Mario Draghi’s report was blunter than usual and highlighted some stark realities for the EU: a fragmentation-driven growth gap with the US, a need for massive investment, a lack of scale tech champions, and an over-regulated, under-capitalised, energy-insecure bloc facing a “slow agony.”

And, along with the other reports, I suspect almost nothing will be done about it. The EU has proven itself incredibly resilient to reform and change.

And this is what I don’t understand about the die-hard remainers. Europe is doing poorly. You can see it in the numbers. The EU even acknowledges that it’s doing poorly, and yet, with all this cultish desire to align, the key question of ‘why?’ remains unanswered.

Brexit gave Britain unilateral control of every lever to avoid this fate. Yet, Westminster prefers to stick close to a failing economic bloc rather than pull these levers. The £100 billion narrative is a convenient shield for inaction and a distraction from the genuine policy choices available to boost our economy.

In my opinion, this is the real failure.

Hardware Fine, Software needs a complete reinstallation

Whitehall can still draft Bills, the Bank of England can still print money, and the courts usually sit on time. The problem isn’t the plumbing in the UK, it’s the people:

Until that human capital upgrade happens, expect more heroic PowerPoints, pointless press releases, more missed investment cycles, and the same chorus of forecasters praying reality will finally match the spreadsheet. The £100 billion narrative is just a symptom of this institutional inertia, a convenient scapegoat for deeper, systemic issues.

Brexit didn’t break the UK economy; it simply exposed who’s running it.

The Elephant in the Room: What Kind of Economy Does Britain Want?

But perhaps the biggest question, largely ignored in the squabble over flawed forecasts, is what kind of economy Britain wants to be. As Michael Pettis recently argued in Politico, the UK has evolved into a consumption-driven economy, where financial services and asset inflation (especially real estate) have replaced industrial employment as sources of income growth. Our openness to global capital, while benefiting the City, has arguably subsidised imports, overvalued the sterling, and undercut British manufacturers.

The risk of Singapore-on-Thames

We can also see that this is where the social-political divide has opened up. People who have benefited from this financialisation of the economy (like me) have largely ignored the costs that others have had to bear.

Learn to lay bricks; the country needs more builders

I am not sure the often-quoted dream of prominent Brexiteers of a ‘Singapore-on-Thames’ is even possible in a country the size of the UK.

The risk now is becoming even more reliant on speculative capital. Do we truly want to remain a nation where a highly paid (and increasingly highly taxed) elite generates financial assets, effectively paying people to do nothing via an ever-expanding welfare state?

This doesn’t look sustainable to me, particularly given the government’s pursuit of low-value immigration and voters’ increased discontent. Or do we want something more balanced, with a revitalised industrial base, more equitable wealth creation, and genuinely productive investment?

This isn't just about economic models; it's about a fundamental choice for the UK's future. Brexit, for all its perceived costs and benefits, has exposed this underlying dilemma. The real challenge is deciding if we're willing to chart a course that prioritises long-term, balanced prosperity over the short-term sugar highs of financial acrobatics and continued reliance on global imbalances.

Unfortunately, by leaving and reducing the flow of investment (which didn’t look sustainable anyway) and not taking any action after leaving to generate higher growth, we appear to have managed the worst of all possible worlds. I believe we are about to be hit by traffic coming both ways.